Predatory Coercion.

The purely selfish kinds of coercion are a form of predatory behavior by the coercing party, whose aim is to narrow down the scope of other people’s actions so as to make them instrumental to its own personal interests. According to many, this sort of predatory behavior will become the prevailing one.

Coercion.

**I wanted to share this, in case you didn't know. Perhaps this will be helpful for you, now and in the future. As a company you are fraught with investigations, perhaps someone should just start giving you the definitions of what you are doing...so you can no longer claim incompetence, or "lost files" or too complicated, or "we didn't know" or

"it was an error"

Here it is in Black and White. Just for you.

Sincerely,

Michelle Hansen of Aurora Colorado

Thursday, August 22, 2013

Wednesday, August 21, 2013

ALERT ALERT!!!!! For $200,000 (plus) We "Might" be able to work with you" Says JPMorgan Chase Executive Office.

"....For $200,000(plus)

We "Might"

be able to work with you."

Says JPMorgan Chase Employee in the Executive Office. August 19th, 2013

"If We Can't, there is No Guarantee that you will get that Money Back."

The bank probably calls this a negotiation of some kind, I however call this something completely different.

-Michelle Hansen of Aurora Colorado

Monday, August 19, 2013

More Investigations into JPMorgan. 7 Ongoing investigations. (I'm seeing a trend)

JPMorgan Chase Energy Trades Under Investigation By DOJ: Report

Posted: 08/19/2013 5:39 pm EDT | Updated: 08/19/2013 7:25 pm EDT

The Wall Street Journal reports that JPMorgan Chase, the country's largest bank by assets, is under investigation yet again, this time by the Department of Justice over its energy trades.

At a minimum, it's the seventh ongoing investigation into the bank, according to the Journal.

Reuters reports:

(Reuters) - JPMorgan Chase & Co is being investigated by the U.S. Department of Justice for possible manipulation of energy markets following the company's settlement of civil allegations last month with a separate federal energy agency, the Wall Street Journal reported on Monday, citing people familiar with the case.

The probe, which was said to be in early stages, is being handled by U.S. Attorney Preet Bharara in Manhattan, the newspaper said on its website. Bharara recently brought criminal charges against two former JPMorgan traders for understating losses from the bank's disastrous London Whale derivatives trades last year.

The Justice Department began the probe of JPMorgan's energy trades as the company agreed to pay $410 million to end an enforcement action by the Federal Energy Regulatory Commission, according to the report, which said the new probe is to include some of the same issues. It is not known if the investigation is civil or criminal, the newspaper said.

A JPMorgan spokesman declined to comment on the report. A Justice Department spokeswoman in Washington had no immediate comment.

Chief Executive Officer Jamie Dimon has publicly vowed to resolve the company's regulatory issues.

**********************************

Shared to you from the Huffington Post

JPMorganChase Continues Mis-Treatment of Michelle Hansen in Aurora Colorado

JPMC You are pretty powerful, not only do you make money appear, and manipulate the cost of energy...and make people power of attorneys without their signature....Now I am a borrower, on a home that you say isn't mine, but demand paperwork that you say you haven't received but in the next line say you will not accept...and say, Yeah we know...but the foreclosure is going to continue.

I think you need help.

If I were a Dr. I would diagnose you as bi-polar, and then I would designate Bank of America to oversee all of your legal endeavors, because you are unfit, and because quite frankly....you deserve that.

I'm so tired of this BS.

I think you need help.

If I were a Dr. I would diagnose you as bi-polar, and then I would designate Bank of America to oversee all of your legal endeavors, because you are unfit, and because quite frankly....you deserve that.

I'm so tired of this BS.

Front Page of the Denver Post. Colorado Foreclosure firm on Hot Seat. **BOOM**

Colorado foreclosure firm on hot seat

PROBE: Whistle-blower alleges law group padded expenses, kept refunds due clients

Attorney fees in foreclosures are unique in that they ultimately are borne by the public, Assistant AG Erik Neusch wrote in a court brief in the Aronowitz case. (Associated Press file)

RELATED STORIES

- Aug 18:

- Foreclosure lawyers charge some homeowners for nonexistent cases

- Aug 10:

- AG: Lawyer e-mails indicate collusion to control foreclosure billing

- Aug 1:

- Denver foreclosure lawyer faces federal sanctions

- Jul 30:

- State's biggest foreclosure law firm fights subpoena for records

- Jul 26:

- Colorado attorney turned whistle-blower alleges foreclosure abuses

- Jul 24:

- Colorado's 2nd-largest foreclosure law firm sued in over-billing probe

- Jul 11:

- Denver judge orders foreclosure lawyer to comply with investigation

- Colorado foreclosure lawyers target of probe into billing practices

- May 25:

- Colorado AG requests foreclosure lawyers' documents from 4 counties

Colorado's second-largest foreclosure law firm allegedly padded attorney expenses, pocketed refunds due its clients and made millions of dollars by running side companies affiliated with its foreclosure work and overcharging for it, a lawyer-turned-whistle-blower has told state investigators.

Susan Hendrick laid out over several meetings with the Colorado attorney general's office a pattern of alleged abuse and misconduct that stretched out for years at Aronowitz & Mecklenburg, the Denver law firm where she was a lawyer, according to documents unsealed in a lawsuit that would have shielded them from public view.

Meanwhile, an Aronowitz employee said in an affidavit that Hendrick admitted to coming forward with personal financial gain as her goal.

Attorneys at the firm were encouraged "to bill the client for more time than was actually spent" on foreclosure cases that homeowners contested in court, according to an affidavit filed by AG investigator Shelly-Jean Sartor, who said she met with Hendrick several times.

The firm charges a flat fee for foreclosures that homeowners did not contest but an hourly fee when they are contested, Hendrick told Sartor.

After several meetings, Hendrick texted investigators that the firm appeared to be hiding its conduct.

"It is my understanding that there is a project underway to clean up a certain problem and that includes the destruction of evidence," Sartor said Hendrick texted her in March.

The law firm "flatly rejects and denies any allegation of inappropriate conduct," its attorney, Richard Benenson, said in an e-mail Friday.

A spokeswoman for Attorney General John Suthers refused to comment.

The unsealed documents provide a clearer picture of what Hendrick told investigators, the first details of which emerged in a Denver District Court hearing last week. Aronowitz argued to seal the case from public view, but District Court Judge R. Michael Mullins disagreed and opened the hearing. Documents in the case file were unsealed Friday.

Hendrick told investigators that other employees at the law firm told her how it improperly charged for title commitments during the foreclosure process, although the investigator's affidavit doesn't detail how.

She also told investigators that employees said the company doesn't refund client money that's advanced to county sheriffs for eviction costs, with any unspent balance later returned.

Sartor said Hendrick told her she had informed partners at the firm about her discoveries — but not about her contacts with investigators.

With regard to the alleged padding of attorney fees, firm partner Stacey Aronowitz "told Hendrick that she was 'onto something' and the law firm tries to shield attorneys from billings so that they have 'plausible deniability,' " Sartor said in an affidavit.

Hendrick said she was asked to help clear up the problems and later was offered $1,000 to sign a confidentiality agreement. She refused to sign.

Investigators say Hendrick contacted them in August 2012 after reading a Denver Post story detailing how county public trustees — the overseers of the state's foreclosure process — were asked to provide investigators with bills that attorneys had filed.

Those bills detail expenses that the lawyers say they're allowed by law to recoup. Investigators have been focusing on charges that lawyers say they paid for the posting of a pair of legal notices informing homeowners of their rights in the foreclosure process.

Investigators found the market rate to post the notices — one telling homeowners about a 90-day deferral they can apply for and the other telling them of a court hearing called a Rule 120 — is about $25 apiece. The lawyers bill up to $150 for each.

The charges are sometimes paid by homeowners if they want to "cure" the deficiency and stop the foreclosure, or by investors seeking to buy the foreclosed property at a public trustee auction.

All the firms revealed to be under investigation — Aronowitz, the Castle Law Group, Vaden Law Firm, Dale & Decker, and the Hopp Law Firm — have tried to shield some of their records from investigators, saying their content is protected by attorney-client privilege.

In denying one firm's request for attorney-client protection of its records, Denver District Judge Edward Bronfin said the privilege is designed to protect clients, not attorneys trying to hide their own misconduct.

"Unlike most attorney billing matters, the foreclosure billing process is unique because the attorney's claimed fees and costs are ultimately borne by the public, not the client," Assistant Attorney General Erik Neusch wrote in a brief to prevent Aronowitz from having the investigation sealed from public view.

Aronowitz posts its foreclosure notices using Xceleron, which is owned entirely by the firm's partners: Robert Aronowitz, his daughter Stacey and his son-in-law Joel Mecklenburg.

Investigators say Xceleron is managed by another of Robert Aronowitz's daughters, whose name is not in court documents.

Investigators also say the partners have made more than $6 million in profits in the venture since 2009, when the Colorado legislature required the postings.

Hendrick worked at the firm until April.

An Aronowitz employee said in a court affidavit that Hendrick said "she was interested in leveraging the firm for a settlement so she could pay off her student loans, fund an IRA and take some time off."

"When I pressed Hendrick that her position sounded like 'extortion,' Hendrick responded by explaining 'that's how it's done,' " Madeleine Daly said in the affidavit.

Neither Hendrick nor her attorney responded to efforts to reach them.

David Migoya: 303-954-1506, dmigoya@denverpost.com or twitter.com/davidmigoya

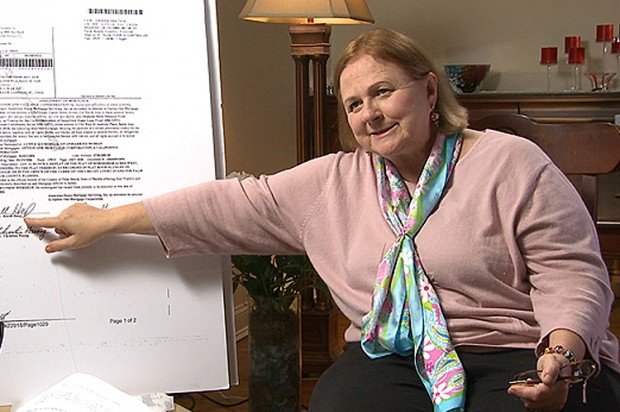

Your Mortgage Documents Might By FAKE. Ofcourse not...Banks Are Honest SAID NO ONE EVER.

Your Mortgage Documents Might be Fake!

Ya think, maybe? MERS alleges to have registered 71 million mortgages. There were likely another 15-20 million “non-MERS” mortgages…

Ya think, maybe? MERS alleges to have registered 71 million mortgages. There were likely another 15-20 million “non-MERS” mortgages…

Lynn Szymoniak in Salon:

BY DAVID DAYENPrepare to be outraged. Newly obtained filings from this Florida woman’s lawsuit uncover horrifying scheme (Update)

BY DAVID DAYENPrepare to be outraged. Newly obtained filings from this Florida woman’s lawsuit uncover horrifying scheme (Update)

If you know about foreclosure fraud, the mass fabrication of mortgage documents in state courts by banks attempting to foreclose on homeowners, you may have one nagging question: Why did banks have to resort to this illegal scheme? Was it just cheaper tomock up the documents than to provide the real ones? Did banks figure they simply had enough power over regulators, politicians and the courts to get away with it? (They were probably right about that one.)

Thom Hartmann talks with Lynn Szymoniak, Attorney / President & Founder-The Housing Justice Foundation. Website: http://thjf.org/, about her efforts to help those who are getting screwed by the big banks.

If you liked this clip of The Thom Hartmann Program, please do us a big favor and share it with your friends… and hit that “like” button!

Continued from Salon:

A newly unsealed lawsuit, which banks settled in 2012 for $95 million, actually offers a different reason, providing a key answer to one of the persistent riddles of the financial crisis and its aftermath. The lawsuit states that banks resorted to fake documents because they could not legally establish true ownership of the loans when trying to foreclose.

This reality, which banks did not contest but instead settled out of court, means that tens of millions of mortgages in America still lack a legitimate chain of ownership, with implications far into the future. And if Congress, supported by the Obama administration, goes back to the same housing finance system, with the same corrupt private entities who broke the nation’s private property system back in business packaging mortgages, then shame on all of us.

This reality, which banks did not contest but instead settled out of court, means that tens of millions of mortgages in America still lack a legitimate chain of ownership, with implications far into the future. And if Congress, supported by the Obama administration, goes back to the same housing finance system, with the same corrupt private entities who broke the nation’s private property system back in business packaging mortgages, then shame on all of us.

The 2011 lawsuit was filed in U.S. District Court in both North and South Carolina, by a white-collar fraud specialist named Lynn Szymoniak, on behalf of the federal government, 17 states and three cities. Twenty-eight banks, mortgage servicers and document processing companies are named in the lawsuit, including mega-banks like JPMorgan Chase, Wells Fargo, Citi and Bank of America.

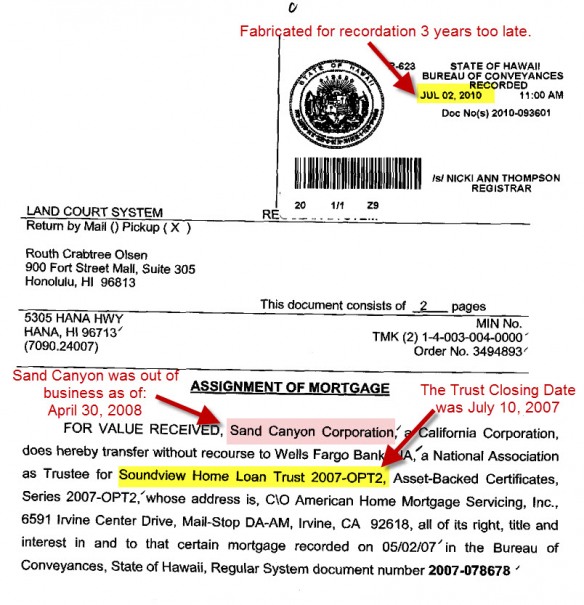

Szymoniak, who fell into foreclosure herself in 2009, researched her own mortgage documents and found massive fraud (for example, one document claimed that Deutsche Bank, listed as the owner of her mortgage, acquired ownership in October 2008, four months after they first filed for foreclosure). She eventually examined tens of thousands of documents, enough to piece together the entire scheme.

A mortgage has two parts: the promissory note (the IOU from the borrower to the lender) and the mortgage, which creates the lien on the home in case of default. During the housing bubble, banks bought loans from originators, and then (in a process known as securitization) enacted a series of transactions that would eventually pool thousands of mortgages into bonds, sold all over the world to public pension funds, state and municipal governments and other investors. A trustee would pool the loans and sell the securities to investors, and the investors would get an annual percentage yield on their money.

In order for the securitization to work, banks purchasing the mortgages had to physically convey the promissory note and the mortgage into the trust. The note had to be endorsed (the way an individual would endorse a check), and handed over to a document custodian for the trust, with a “mortgage assignment” confirming the transfer of ownership. And this had to be done before a 90-day cutoff date, with no grace period beyond that.

Georgetown Law professor Adam Levitin spelled this out in testimony before Congress in 2010: “If mortgages were not properly transferred in the securitization process, then mortgage-backed securities would in fact not be backed by any mortgages whatsoever.”

Georgetown Law professor Adam Levitin spelled this out in testimony before Congress in 2010: “If mortgages were not properly transferred in the securitization process, then mortgage-backed securities would in fact not be backed by any mortgages whatsoever.”

The lawsuit alleges that these notes, as well as the mortgage assignments, were “never delivered to the mortgage-backed securities trusts,” and that the trustees lied to the SEC and investors about this. As a result, the trusts could not establish ownership of the loan when they went to foreclose, forcing the production of a stream of false documents, signed by “robo-signers,” employees using a bevy of corporate titles for companies that never employed them, to sign documents about which they had little or no knowledge.

Many documents were forged (the suit provides evidence of the signature of one robo-signer, Linda Green, written eight different ways), some were signed by “officers” of companies that went bankrupt years earlier, and dozens of assignments listed as the owner of the loan “Bogus Assignee for Intervening Assignments,” clearly a template that was never changed. One defendant in the case, Lender Processing Services, created masses of false documents on behalf of the banks, often using fake corporate officer titles and forged signatures. This was all done to establish standing to foreclose in courts, which the banks otherwise could not.

Szymoniak stated in her lawsuit that, “Defendants used fraudulent mortgage assignments to conceal that over 1400 MBS trusts, each with mortgages valued at over $1 billion, are missing critical documents,” meaning that at least $1.4 trillion in mortgage-backed securities are, in fact, non-mortgage-backed securities. Because of the strict laws governing of these kinds of securitizations, there’s no way to make the assignments after the fact. Activists have a name for this: “securitization FAIL.”

One smoking gun piece of evidence in the lawsuit concerns a mortgage assignment dated Feb. 9, 2009, after the foreclosure of the mortgage in question was completed. According to the suit, “A typewritten note on the right hand side of the document states: ‘This Assignment of Mortgage was inadvertently not recorded prior to the Final Judgment of Foreclosure… but is now being recorded to clear title.’”

One smoking gun piece of evidence in the lawsuit concerns a mortgage assignment dated Feb. 9, 2009, after the foreclosure of the mortgage in question was completed. According to the suit, “A typewritten note on the right hand side of the document states: ‘This Assignment of Mortgage was inadvertently not recorded prior to the Final Judgment of Foreclosure… but is now being recorded to clear title.’”

This admission confirms that the mortgage assignment was not made before the closing date of the trust, invalidating ownership. The suit further argued that “the act of fabricating the assignments is evidence that the MBS Trust did not own the notes and/or the mortgage liens for some assets claimed to be in the pool.”

The federal government, states and cities joined the lawsuit under 25 counts of the federal False Claims Act and state-based versions of the law. All of them bought mortgage-backed securities from banks that never conveyed the mortgages or notes to the trusts. The plaintiffs argued that, considering that trustees and servicers had to spend lots of money forging and fabricating documents to establish ownership, they were materially harmed by the subsequent impaired value of the securities. Also, these investors (which includes the Treasury Department and the Federal Reserve) paid for the transfer of mortgages to the trusts, yet they were never actually transferred.

Finally, the lawsuit argues that the federal government was harmed by “payments made on mortgage guarantees to Defendants lacking valid notes and assignments of mortgages who were not entitled to demand or receive said payments.”

Despite Szymoniak seeking a trial by jury, the government intervened in the case, and settled part of it at the beginning of 2012, extracting $95 million from the five biggest banks in the suit (Wells Fargo, Bank of America, JPMorgan Chase, Citi and GMAC/Ally Bank). Szymoniak herself was awarded $18 million. But the underlying evidence was never revealed until the case was unsealed last Thursday.

Now that it’s unsealed, Szymoniak, as the named plaintiff, can go forward and prove the case. Along with her legal team (which includes the law firm of Grant & Eisenhoffer, which has recovered more money under the False Claims Act than any firm in the country), Szymoniak can pursue discovery and go to trial against the rest of the named defendants, including HSBC, the Bank of New York Mellon, Deutsche Bank and US Bank.

Now that it’s unsealed, Szymoniak, as the named plaintiff, can go forward and prove the case. Along with her legal team (which includes the law firm of Grant & Eisenhoffer, which has recovered more money under the False Claims Act than any firm in the country), Szymoniak can pursue discovery and go to trial against the rest of the named defendants, including HSBC, the Bank of New York Mellon, Deutsche Bank and US Bank.

The expenses of the case, previously borne by the government, now are borne by Szymoniak and her team, but the percentages of recovery funds are also higher. “I’m really glad I was part of collecting this money for the government, and I’m looking forward to going through discovery and collecting the rest of it,” Szymoniak told Salon. [Read more on Salon]

Big thanks to Shelley for highlighting this post and video – and kudos to Lynn for all the good work she does.

Michelle Hansen Files 3 Different Complaints to the Powers that Be. Anyone Paying Attention Yet?

Here we go.

I'm tired of being lied to...empty promises, bad faith, and the run around and other shenanigans.

JPMorgan Chase, I'm not playing your corrupt game.

You can take your Bait and Switch crap and put it.....

Michelle

I'm tired of being lied to...empty promises, bad faith, and the run around and other shenanigans.

JPMorgan Chase, I'm not playing your corrupt game.

You can take your Bait and Switch crap and put it.....

Michelle

JPMorgan Chase Says For 200+K We "Might" Work with You Michelle Hansen.

JPMorgan Chase will need me to trust them with a payment of 200k+ and then they "might" be able to work with me, but they cannot guarantee that, and the payment is non-refundable.

I don't know why I wouldn't trust them...Here is their rap sheet...off the top of my head.

Being Investigated for Bribery.

Mortgage Fraud

Robo-signing. Falsifying Documents

Committing Fraud on the Courts.

Fraud in Federal Bankruptcy Court.

Federal Criminal Fraud Charges

Criminal Charges on Falsifying their Books

Criminal Fraud Charges with the "London Whale"

fraudulent and unlawful debt-collection practices

Energy Manipulation

Wrongful Death

hmmm, now I'm not a banker...but what do you think the risk ratio would be on this bet.

I don't know why I wouldn't trust them...Here is their rap sheet...off the top of my head.

Being Investigated for Bribery.

Mortgage Fraud

Robo-signing. Falsifying Documents

Committing Fraud on the Courts.

Fraud in Federal Bankruptcy Court.

Federal Criminal Fraud Charges

Criminal Charges on Falsifying their Books

Criminal Fraud Charges with the "London Whale"

fraudulent and unlawful debt-collection practices

Energy Manipulation

Wrongful Death

hmmm, now I'm not a banker...but what do you think the risk ratio would be on this bet.

Subscribe to:

Comments (Atom)